Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Dallas Federal Reserve President CSPAN January 19, 2013 12:05pm-1:00pm EST

12:05 pm

tbtf. i submit that these institutions exact unfair taxes on the american people and they interfere with the transmission of monetary policies, which is my business, and inhibit the advancement of economic prosperity. i spoke on this for several years. i began with a speech in july of 2009 entitled "the pathology of too big to fail." i and our staff have written about it extensively. tomorrow, we will be issuing a special report available on the net that further lessen our proposal. it addresses the performance of community banks and regional breaks during the raid -- during the recent crisis.

12:06 pm

i want to urge you all to access that report when we make it public mar. the federal reserve convention requires that i issued a disclaimer, which is that i only speak for the federal reserve bank of dallas. not for any other association with our great central bank. this is usually abundantly clear. [laughter] but i have to say that. in many matters we entertain opinions that are very much different than those of our esteemed colleagues. i was the fourth my sentiments freely and without reserve on the issue of too big to fail. i mean no disrespect to others to harbor different views. everyone and their sister knows that the financial institutions that are too big to fail are at the epicenter of the two thousand nine financial crisis. they are known as islands of

12:07 pm

safety. they became agents and fight -- agents and enablers of the financial tsunami. we at the dallas fed said mitt they are the key reason that the accommodative monetary policy and government policies have failed to adequately affect economic recovery. we first wrote an article about this in "the wall street journal" in 2009. put simply, sick banks do not lend. mega banks stop their lending in the capital markets' activity during the crisis of economic recovery. they brought economic growth to a standstill. and then they spread their sickness to the rest of the banking system. congress thought it would address that matter through what is known as the dodd-franc wall street -- the dog frank wall street protection act. -- the dodd-frank wall street

12:08 pm

protection act. we can test it had that done enough. -- it had not done enough. it exacerbated economic growth by a -- it has benefited many. they are known as lawyers. it has created many new levels of bureaucracy. we believe it has been counterproductive in working against the core problems it seems to address. let me define what i mean when i say to big to fail. the definition is financial firms whose owners, managers, and customers believe themselves to be exempt from the process of bankruptcy. said firms captured the financial upside of their actions but they largely avoided

12:09 pm

payments for actions gone wrong. a violation of one of the basic tenets of capitalism. subsidies relative to their non -too big to fail competitors, the create a risk in profits, protected by the presumption that bankruptcy is highly unlikely to obtain. the phenomenon of too big to fail resulted in a widely taken for granted government sanction, coming to the aid of managers and creditors of financial institutions deemed too large and so interconnected and complex that its failure could substantially damage the financial system. systemically important financial says -- financial institutions. such policies undermine the discipline that market forces normally assert unmanaged decision making.

12:10 pm

it has been further eroded by composite extension of the federal safety net beyond commercial banks that are not bank affiliate's. moreover, industry consolidation fostered by subsidize growth in the crisis encouraged outright by the federal government's have further perpetuated and enlarged the weight of financial firms deemed too big to fail or to systemically important. that result is it reduces competition and landing. dodd-frank does not do enough to constrain the behemoths bank advantages. indeed, give it its complexity it unwittingly exacerbates them. a highly respected member of the bank of england addresses in a very witty speech -- here are

12:11 pm

some choice passages. "efforts to catch the crisis frisbee have continued to escalate." "the frisbee catching abilities -- no light and later had the foresight to predict the financial crisis. some have exhibited supernatural powers of hindsight. " what is the secret to the watchdog's failure? the answer is simple in its complexity. complex regulation might not come% but sub-optimal. -- cumbersome but sub-optimal. he had a great quit after president wilson presented his 14 points. "for why 14? god didn't intend."

12:12 pm

-- god did it in 10." he points out that in 1986 the reports received from banking companies, it covered 74 columns of excel reporting. excel has expanded sufficiently to capture those increases. dodd-frank has layered on copious amounts of the complexity. the legislation as everybody knows has 16 titles and runs 849

12:13 pm

pages. more than 8800 pages of regulations have been proposed and the process is not yet done. in his speech, he noted that in a survey of the federal register that applies to these new rules to hundred -- the cost of this regulatory oedipus' would be small -- of this -- the week is certainly not worth the candle. he concludes, "modern finance is complex. almost certainly too complex. that configuration spells trouble as he did not fight fire with fire. you did not fight complexity

12:14 pm

with complexity. the situation requires a regulatory response, not complexity. delivering that would require an about turn be " well, the dallas federal reserve's proposal offers an about turn in a way to amend the flaws of dodd-frank. it fights complexity with simplicity where appropriate. it eliminates the mumbo jumbo complexity of dodd-frank. it would be especially helpful for the knot -- for the non-too big to fail banks. our proposal would relieve small bags of unnecessary burdens that unfairly penalizes them. our proposal would effectively level of playing field for all banking organizations in the country. it would provide the best protection for taxpaying citizens. in a nutshell we recommend too big to fail institutions be

12:15 pm

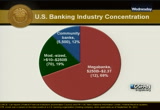

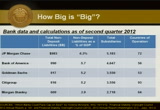

restructured into multiple business entities. only the down side resulting commercial banking accommodations, not the parent companies, would benefit from the safety net of deposit insurance or from access of the federal reserve window. it is important to evaluate this against an understanding of the landscape of banking today. here is a little chart. as of the third quarter of 2012 there are approximately 5600 commercial banking organizations in the united states. the bulk of these are 5500 community banks with less than the 10 million. another group numbering nearly 70 banking organizations, those of the green cards there, they

12:16 pm

estimate between $10 billion to $250 billion. they control 90% of the industry's assets. the mega bank's assets between two and $50 billion and two 0.3 trillion dollars, it is made up of a mere 12 institutions. accountzen behemoth's for roughly 0.2% of all banks. but they hold 69% of all of the assets for the industry. the 12 institutions that are presently accounting for -- our candidates considered too big to fail because of the threat they posed to the financial system. by contrast, should the other 99.98% of banking get into trouble they would be most likely end up with private sector changes and minimal government intervention. how and why this works for

12:17 pm

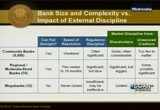

99.8%, but not for the other 0.2% -- it helps to consider the sources of regulatory market discipline imposed on each of these three groups of banks. we allow it to the image of regulatory discipline, potential the -- potential closure and bank management practices. it is summarized in this slide that i hope this behind me as i speak. it is clear the community banks are subject to considerable regulatory and shareholder disciplined. they can and do fail. in the last few years the fdic has filtered repetition for regulators carrying out -- on friday -- in on friday, out on monday. knowing the power of banks to

12:18 pm

divisors to close the institution, owners and managers of community banks he'd supervisory recommendations against risk. supervisory recommendations against risk. they exert substantial control over the behavior of management, as risk and potential enclosure matter to them. -- risk and potential closure matter to them. they are simple rather than complex in the capital structure. they really have uninsured creditors. market discipline, over management practice, is primarily exerted through that limited number of shareholders. of the three groups shown on this slide, the 70 regional and moderate sized organizations are subject to a broader range of market discipline. like community banks, these institutions are not exempt from the bankruptcy process. they can and do fail.

12:19 pm

given their size and complexity, the failure resolution and transfer cost as cannot become accomplished over -- transfer process cannot be accomplished over a weekend. uninsured depositors and unsecured creditors are also aware of their unprotected status in the event the institution experience financial difficulties. midsized banking institutions receive a good dose of external discipline from both supervisors and market-based signals. on the other hand, the mega banks, the too-big-to-fail megabanks, received far too little regulatory discipline. for all intents and purposes we believe these banks have not been allowed to fail outright. knowing that, the management of

12:20 pm

these banks can, and to a large extent do it, choose to resist the advisement of their managers. let me first walking through the discipline for shareholders. if you have millions of shareholders you that the shareholders' ability to manage the too big to fail banks from pursuing corporate strategies that are profitable for management but not necessarily for shareholders. as we learned during the crisis, it is too late for shareholder reaction or spreads to have any mitt -- any impact on management behavior. during the financial crisis, shares of the two largest bank holding companies declined by 95% from their peak prices and their credit defaults went

12:21 pm

haywire. even though the decisions that led to that market reaction occurred well ahead of them. agencies eventually reacted. the damage from excessive risk- taking had already been done. after the crisis, judging from the behavior of many but not all of the largest bank holding companies, with limited exception -- efforts by shareholders of these institutions to meaningfully influence management compensation practices were called back and have been very slow in coming. so much for shareholder does plan to check on too big to fail banks. unfortunately these banks do not face much external discipline from the unsecured creditors. an important facet of too big to fail is funding source for my

12:22 pm

banks extend way beyond their insured deposits. it is referred to credit defaults swaps. the larger banks find themselves with a wide range of liabilities. these include large negotiable c.d.s, which often exceed the term limit. federal funds purchased from other banks, all of which are uninsured, and notes and bonds generally unsecured. it is not unusual for on the secured liabilities -- for unsecured liabilities to compile over half of the liabilities. one would expect it to come from unsecured and uninsured depositors. creditors and the debt holders. but, too big to fail status asserts what we call a perverse market discipline on the risk- taking activities of these banks. unsecured creditors recognize the government guarantee that

12:23 pm

they have on their liabilities. as a result, unsecured depositors and creditors offer their funds at a lower cost. the two big to fail banks have to midsize and the regional bank's rate -- regional banks face the risk of failure. the subsidy is quite large and it has risen following the recent financial crisis. recent estimates by the international settlements suggest that the implicit government guarantee provides the largest bank holding companies with an average credit rating uplift of more than two notches. thereby lowering their average funding costs. my aforementioned friend at the bank of england encourage the implicit too big to fail subsidies to be roughly $3 billion per year for the 29 global restitutions defined by the stability board as systemically important. to put that $300 billion in

12:24 pm

perspective, that is an annual subsidy, all of these u.s. holding companies coming together reported a $8 billion in 2011. here's a basic chart for a typical financial holding company. to simplify complex structure, one might consider all of the operations done in the commercial banking operation, that was a box and the bottom left over my shoulder. all other operations are what you could call a shot of making -- shadowed-banking affiliates. consider this next table. it gives you a size and sense of scope for the five largest banking companies. note there is not deposit liabilities in the billions of dollars. the total subsidiaries --

12:25 pm

for perspective, let us consider this case. the resolution is not yet over. and yet the offer two of its 39 subsidiaries according to their last filing. -- they offered 239 subsidiaries according to their last filing. it was too big for a private sector to find a resolution. what can be inferred from the big five on the table over my shoulder? .for addresses this concern. the systemically important financial' institution would receive financing from the u.s. treasury in order to stabilize. by our view of the dallas fed this is causing the

12:26 pm

nationalization. in dallas to consider government ownership of our financial institutions, even on a temporary basis, to be a clear distortion of american capitalist principles. an alternative would be to have another systemically important institution acquire a failing institution. we have already been down that road. all it does is compound the problem. expanding the risk posed by even larger surviving behemoths organizations. the practice of arranging shotgun marriages between giants worsens the funding disadvantage of the 99.8% remaining regional banks. it favors the unwieldy and dangerous too big to day -- too big to fail banks over a more disciplined banks. the approach of the dallas fed, as ed explained earlier, neither expands the reach of government

12:27 pm

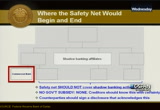

nor further handicaps the 99.8% of regional banks. nor does it by complexity with complexity. it simply calls for a reshaping of the too big to fail financial institutions into smaller, less complex institutions that are economically viable, profitable, competitively able to attract capital, and are of a size, complexity, and scope for regulatory and market is a plan. -- market discipline. it can be accomplished with minimum statutory modification. it can be implemented with as little government intervention as possible. it calls first for rolling back the federal safety net. second, it calls for clarifying to simple and understandable disclosures that the federal safety net only applies to

12:28 pm

commercial banks and its customers and never ever to customers of any other affiliated subsidiary or holding company. they must never received taxpayer support. we recognize that and doing customer inertia and -- for these reasons it may be that additional action is necessary. too big to fail bank holding companies may need to be downsized and restructured so that the safety net supporting the commercial part can be disciplined by regulators and market courses. there will likely have to be additional prohibition on the ability to remove assets from the shadow banking affiliates to the banking affiliates within the holding company. we saw some of that take place

12:29 pm

turned crisis, it should not have happened. to illustrate how the first two points of our plan worked, i come back to the hypothetical structure of holy cap the. -- of holding capital. these are legitimate, the operations. they should be allowed to operate. but not with government guarantees. our proposal is that only the commercial banks would have access to the process. only the commercial bank would have access to the discount window loans provided by my organization and federal reserve. these two features of the safety net would explicitly by statute become unavailable to any shadow banking affiliates. theoretically this is current

12:30 pm

practice. and yet practice -- in practice it has not been so. to reinforce the statute and its credibility every customer, a creditor, and counterparty of every shadow banking affiliate and senior bank holding company would be required to agree to and signed a new covenant. a simple disclosure statement that acknowledges there are protected status. you can read as i do. it is one paragraph. "conducting business with this affiliate's of the holding company carries no deposit or other federal protection guarantees. i fully understand the conducting business with the john henry banking affiliate have no federal deposit insurance from other -- or federal protection guarantees.

12:31 pm

this two part step should begin to remove the too big to fail holding companies and their shadow banking operations. these commercial banks have an appropriately benefited from a safety net. our proposal promotes competition in light of market and regulatory discipline, replacing the status quo subsidize a personal banking to take risks. some government intervention may be necessary to accelerate the imposition of affect of market discipline and bridge this practice. we believe market forces should be relied on as much as is practical. it is true that entrenched forces and entrenched regulatory forces, in combination with customer and their ship, will likely only be overcome through government sanction and restructuring of too big to fail bank holding companies. the subsidy is impossible to

12:32 pm

take away. we may need a push. my team at the dallas fed and i are confident. think about it this way. if 99.8% of banking organizations are subject to market disciplines to contain the risk of misbehavior that can threaten the financial system of the american and global economy, 0.2% are not. their very existence threatens both economic and financial stability. and furthermore, to contain that risk, of regulators and many small banks are tied up in regulatory and legal knots in an enormous indirect and direct

12:33 pm

cost to them and the economy. 0.2%. if the administration and congress can agree on legislation that affects the 1% surely they can process a solution that affects the 0.2%. our view is that the time has come to change the decision making paradigm. there should be more than the two present solutions, bailout or the end of the world of the economy as we know it. the next financial crisis could cost more to -- more than two years of economic health and would be borne by more than 2 million extra u.s. taxpayers.

12:34 pm

the remedy is obvious. reintroduce market forces and level the playing field for all banking institutions. i am going to close by returning to patrick hence -- to patrick henry. "it is natural man to indulge -- it is natural for man to indulge in the illusion of hope." today we labor under the song of dodd-frank and the recent run-up of bank stocks and credit, indulging the deletion of hope that this complex legislation will and too big to fail and write the banking system. we shut our eyes to the painful truth that too big to fail represent an ongoing danger. not just affect stability, not just unfair competition, but to the american way. the dallas federal reserve bank

12:35 pm

offers a modest but far more effective fix to dodd-frank. it is less costly than the it -- is less costly than the alternative tweets seen before. it reduces the likelihood of another horrendous and cosset financial crisis this need not be a time of -- it should be a time of promise. trading the pathology of the two big to fail would be a big step forward for the economic system. one that relies on the fundamental principles of capitalism off rather than on regulatory complexity and increasing government intervention. thank you for being tolerant. i would be happy to avoid answering any questions you may have. [laughter] thank you. [applause]

12:36 pm

is one of you guys going to be handling questions? >> i did ask the first question as the first one to sign the affidavit. you mentioned the politics -- or the restructuring that will have to take place. you pointed out the difficulty of the politics. to paraphrase shakespeare, hath no fury like a subsidy scorn. what are the politics on capitol hill? this would require some congressional action, the more the better politically and democratically. what is a look like on capitol hill? >> this is not a regulatory issue, we operate as regular editors at the command of our lawmakers. it is a political issue.

12:37 pm

there are several dimensions of this. you have to get those that make the laws of the united states on your side. i view this as a win-win for both sides. the most powerful force in the country, if they were to exercise their muscle, are the community bankers. there are thousands upon thousands of them. they know every member of the legislature because they helped them get started. they know who they sleep with, drink with, what their habits are. it is their interest to no longer be placed at a disadvantage in terms of funding. nor the competitive disadvantage of knowing that if they screw up, there will be worse than we have been. they live by these principles. it is not there. i do think there is considerable political muscle that can be exercised here. it is appealing to the left, if

12:38 pm

you consider the left being democratic. others have expressed a favorable views towards this approach. i realize the latter is no longer in the senate but i think he represents a point of view that some people might say -- team would not have been in favor of this. -- he would not have been in favor of this. i think it is appealing. the difficulty is replacing complexity with simplicity. winston churchill had a great quote. everything that is agreeable is on sound and everything that is agreeable is unsound. -- everything that is agreeable is unsound and everything that is sound is generally

12:39 pm

disagreeable. favoritism for large financial institutions will not hold. i believe you might have support in the executive, but it has to come from the commerce. they make the laws. they have created this massive thing called dodd-frank only part way through in terms of interpreting. i believe with community bankers parts we will be supported on this issue. this is something we have been bird dogging. i do think it is gaining momentum. as i said earlier, who has

12:40 pm

benefited from this? lawyers and bureaucrats. john? >> i am half australian. thank you for leading me on this. as you know better than me, god and frank would say we dealt with too big to fail and we meant it. --.and frank would say -- we really mean it as regulators. and that is not sufficient to the bankers or the market. i am curious, the party didn't emphasize, the backdrop, what is the plan for government

12:41 pm

intervention to separate the smaller institutions. the second component is your thoughts on emerging problem of too big to jail. government prosecutors decided not to read it decided to defer prosecution for company they alleged was facilitating drug- trafficking and alleged terrorist activity. they thought to prosecute the company with the two systemic risks and to great danger for the world economy. in that light, doesn't seem logical that if a prosecutor makes that informed decision based on conversations with regulators that there should be a defacto paul -- a fact a follow-up? we know it should not be

12:42 pm

permitted to exist in their current form. >> the second question appears to be a statement so i will not answer it. let me answer the first question. senator dodd is spending his time in hollywood. congressman frank is no longer in the congress. how you and do something that has taken so much time to put together? what is the legislative process and how do we get done? was that your question? the markets have already indicated a taste for this. since we first published the article that i referred to we have received enormous support from the bill that made at morgan stanley what it is today

12:43 pm

from mr. stevens in arkansas. and my great surprise, the fellow that started it all at city group. -- and citigroup. i see an outpouring of support for this. i think it is important for them to understand that this is part of a problem as to why we did not recover as quickly as possible. i refer to that in passing. i wrote a great deal about it. it is pretty simple but if you are a manager of a large institution and you have a massive portion of the industry's assets, it is hard for you to focus on your business to become too complex. there is an issue of scale.

12:44 pm

i submitted and written about this in a great deal, one of the reasons we have not clicked as quickly as possible in recovering from the crisis is because the transition mechanism for monetary policy is gummed up. think about it as sludge on the motor of your engine. we provide the fuel. it has to be transmitted into the economy. we not only have to in send people to step on the accelerator to create more jobs, that is a matter of writing jobs, the galatians, tax incentives, and so on, but it has to be trusted to the banking system.

12:45 pm

they are interfering with the effectiveness of the much -- of the economy to water policy. i believe the support is gaining ground. it is not just a question of fairness. it is a question of efficacy. i believe it is beginning to gain ground. [indiscernible] how easy it in a clean fashion? >> that is up to the people on the hill. take that simple language i have, it would take a sixth grader to read it. -- a sixth grader to write it. >> thank you for being us -- thank you for being with us this evening. i would like to give you the

12:46 pm

opportunity to clarify the proposal that i gathered the dallas fed is going to put on as website mar. i look forward to analyzing and writing about it. the problems you are discussing, i have commonly heard remedies of one falling the glass deal approach and separating activities from the banks. isolate the commercial bank activity from everything else. the second is to put a size cap on the commercial banks. do i correctly understand that you and your colleagues at the dallas fed have thought about this and rejected them in favor of the proposal you are now advancing? and if so, can you amplify a bit on the reasons why you think

12:47 pm

they are a bad idea. >> i think the industry has changed from when i was a banker. the owners for all of the risk personally. we found from the old mentality that commercial banks were balanced driven. you are disciplined internally and externally to make sure your pet -- your deposits for protected and intermediate it posed short-term loans. it was a balance-sheet and driven industry. -- a balance-sheet driven industry. i ran a hedge fund for years. i cared about what i made every year. it was a different culture than

12:48 pm

what i experienced as a banker i am not sure we can stuff dodd- frank back in to the bottle. our teams are not saying and i am not saying that the holding companies can engage in these activities. what i am saying is they will not have government guarantees. they will not be able to bar from the discount window. plain and simple. so it does not forbidding, it does not formally split, it implies the guarantees only to a specific practice. and to none of the rest it would be made extremely clear. my colleagues at the board of governors has talked about that. i will leave it up to him in terms of his responsibilities in

12:49 pm

trying to implement data frank. i think he has been quite frank in doing so. i am a little reluctant tooth artificially engineer size. -- reluctant to artificially engineer sides. i did not want to inhibit success. what i do want to prevent is placing the american taxpayer at risk. that is where government intermediacy is. they decide how much money we take and how much we spend. we can argue about that constantly. but to leave unlimited liability open to the american taxpayer for bad decisions taken in the pursuit of an income steven -- an income-statement driven mentality seems to be

12:50 pm

unjust. we have proposed a very simple solution. you begin to see people shed these businesses already. you saw that because a lot of the more complex traditions -- i have faith in the market. the rules are hyper complex and still enormously murky. i think it is very hard to figure out which end is upi can tell ou. i can tell you in our own case this is a very complicated process. ours is an effort in simplicity, fairness, and just making clear that the american taxpayer is only liable for a specific

12:51 pm

practice. no more complex than that. >> i am a customer and shareholder in bank of america. none of bank of america's published reports or documents give me any indication as to what their real assets and liabilities are. i suspect that their balance sheet is laden with tier 3 assets representing customer accommodation in the form of complex derivative transactions that allocate trillions of dollars on the basis which hopefully nets out and gives the bank of much higher return than your commercial bank. is there assurance that this

12:52 pm

disclaimer would apply to all counter parties so the 75 trillion dollars would be a private-sector risk and i, the depositor, would not be exposed because my fear is the bank of america is going to play chicken. we can make money on these very risky tear-3 transactions. if a counterparty freezes, what happens? >> that is exactly the proposal. to prevent that from happening. will the market unwind these horrible exposures? it is up to the market to define. you are a customer. and i do not believe that you

12:53 pm

directly as a taxpayer should be placed at risk for those derivative transactions. you can conduct those irresponsibly. you should not be guaranteed by the federal government if you make a mistake and lawyers. that is all we are saying. that simple declaration, which any sixth grader could read and understand, would be signed by anybody in the top party. you nailed it. that is why you are chairman of this organization. [laughter] [indiscernible] >> we do our best as regulators to make that possible. i will report that back to my colleagues. [laughter] let me thank you for letting me speak year.

12:54 pm

it is an honor. i told my wife that i was speaking at the national press club. i mentioned the other people that have spoken here and i said, "in your wildest dreams did you ever think i would be at a podium in front of this crew?" their response was, "richard, we have been married 40 years. you do not appear in my wildest dreams." [laughter] thank you for having me here. [applause]

12:55 pm

>> we are bringing you the sights and sounds of the inauguration weekend from the capital. president obama will be sworn in on the west side of the capitol building here. you can see the guard rails and barriers that are up to guide ticket holders to their places on monday. we have been showing events related to today's date service. -- day of service. just take a look here at some of the people outside of the capital.

12:56 pm

>> this, of course, the site of president obama's public swearing in. the officials wearing in taken place on sunday as mandated by the constitution. we will bring you live coverage starting at 10:30 a.m. tomorrow. in the meantime we will take a look at the country's inaugural ball. >> welcome to the national building museum. i am a volunteer tutor guide for the museum. we are here today to go through what we call the presidential inaugural taurus. we do this every four years at inauguration time. this building was built as a federal office building over 120

12:57 pm

years ago turned out to be a wonderful place to have the inaugural balls. inaugural balls go back to george bush -- to george washington in 1789. at that time the capital was in new york city. the party was there. by 1793 when he was reelected, the party moved to philadelphia. by that time, washington had been identified as the capital city. this was not a place to do that. he liked parties. martha was not there because she was in mount vernon. but the time john adams became president he decided he would have no party said hall -- no parties at all. the first all we know of was in this town.

12:58 pm

the first party they had was in a hotel. in the succeeding years they had parties and it would collet sometimes a paul, sometimes a party. it wasn't until the late 1840's that it began to get into the theme of having an event of special nature here. they started to build temporary buildings for part of that. one of the things about the inauguration -- the constitution is clear about -- it's as explicitly that on january 20 at noon. there is the appointed allegiance.

12:59 pm

>> i ronald reagan do solemnly swear. that i will faithfully execute the office of president of the united states and will to the best of my ability preserve protect and defend the constitution of the united states. so help me god. [applause] >> the rest of the inaugural events are up to the president's staff. lately it has been a pattern in which the president, after being sworn in, gives the inaugural speech, he then comes to the white house down pennsylvania avenue in a parade. avenue in a parade.

499 Views

IN COLLECTIONS

CSPAN Television Archive

Television Archive  Television Archive News Search Service

Television Archive News Search Service

Uploaded by TV Archive on